Loading required package: car

Loading required package: carData

Attaching package: 'car'

The following object is masked from 'package:dplyr':

recode

The following object is masked from 'package:purrr':

some

Loading required package: effects

lattice theme set by effectsTheme()

See ?effectsTheme for details.

Code

data("florida")

For the house.selling.price.2 data the tables below show a correlation matrix and a model fit using four predictors of selling price.

In this data, the variables are meant as:

P: selling price

Be: number of bedrooms

Ba: number of bathrooms

New: whether new (1 = yes, 0 = no)

Here is my impression of the correlation matrix:

Code

cor(house.selling.price.2)

P S Be Ba New

P 1.0000000 0.8988136 0.5902675 0.7136960 0.3565540

S 0.8988136 1.0000000 0.6691137 0.6624828 0.1762879

Be 0.5902675 0.6691137 1.0000000 0.3337966 0.2672091

Ba 0.7136960 0.6624828 0.3337966 1.0000000 0.1820651

New 0.3565540 0.1762879 0.2672091 0.1820651 1.0000000

And regression output:

Code

fit <-lm(P ~ ., data=house.selling.price.2)summary(fit)

Call:

lm(formula = P ~ ., data = house.selling.price.2)

Residuals:

Min 1Q Median 3Q Max

-36.212 -9.546 1.277 9.406 71.953

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -41.795 12.104 -3.453 0.000855 ***

S 64.761 5.630 11.504 < 2e-16 ***

Be -2.766 3.960 -0.698 0.486763

Ba 19.203 5.650 3.399 0.001019 **

New 18.984 3.873 4.902 4.3e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 16.36 on 88 degrees of freedom

Multiple R-squared: 0.8689, Adjusted R-squared: 0.8629

F-statistic: 145.8 on 4 and 88 DF, p-value: < 2.2e-16

Automated variable selection

For backward elimination, which variable would be deleted first? Why?

If I was doing backward elimination, I would pick a significance level (let’s say alpha = .05) and, at each stage, delete the variable with the largest p-value. I would stop when all variables are significant.

In this example, I would delete the Be (bedroom) variable.

Code

summary(lm(P ~ . - Be, data=house.selling.price.2))

Call:

lm(formula = P ~ . - Be, data = house.selling.price.2)

Residuals:

Min 1Q Median 3Q Max

-34.804 -9.496 0.917 7.931 73.338

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -47.992 8.209 -5.847 8.15e-08 ***

S 62.263 4.335 14.363 < 2e-16 ***

Ba 20.072 5.495 3.653 0.000438 ***

New 18.371 3.761 4.885 4.54e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 16.31 on 89 degrees of freedom

Multiple R-squared: 0.8681, Adjusted R-squared: 0.8637

F-statistic: 195.3 on 3 and 89 DF, p-value: < 2.2e-16

For forward selection, which variable would be added first? Why?

Like backward elimination, I would also predetermine a significance level (say, 5%). But here I would begin with no explanatory variable.

The Size variable would be added first in forward selection.

Code

intercept_only <-lm(P ~1, data=house.selling.price.2)step(intercept_only, direction ="forward", scope=~ S + Be + Ba + New)

Start: AIC=705.63

P ~ 1

Df Sum of Sq RSS AIC

+ S 1 145097 34508 554.22

+ Ba 1 91484 88121 641.41

+ Be 1 62578 117028 667.79

+ New 1 22833 156772 694.99

<none> 179606 705.63

Step: AIC=554.22

P ~ S

Df Sum of Sq RSS AIC

+ New 1 7274.7 27234 534.20

+ Ba 1 4475.6 30033 543.30

<none> 34508 554.22

+ Be 1 40.4 34468 556.11

Step: AIC=534.2

P ~ S + New

Df Sum of Sq RSS AIC

+ Ba 1 3550.1 23684 523.21

+ Be 1 588.8 26645 534.17

<none> 27234 534.20

Step: AIC=523.21

P ~ S + New + Ba

Df Sum of Sq RSS AIC

<none> 23684 523.21

+ Be 1 130.55 23553 524.70

Call:

lm(formula = P ~ S + New + Ba, data = house.selling.price.2)

Coefficients:

(Intercept) S New Ba

-47.99 62.26 18.37 20.07

Why do you think that BEDS has such a large P-value in the multiple regression model, even though it has a substantial correlation with PRICE?

As pointed out, Be does have a substantial correlation with P at .59. However, the large P-values in multiple regression indicate that while holding other variables fixed, it does not ‘explain’ the response variable of P, price.

Using software with these four predictors, find the model that would be selected using each criterion:

I’m not sure if I exactly get the question, but I will arbitrarily compare some models that I have made from combinations of the predictors.

Code

mod1 <-lm(P ~ S, data=house.selling.price.2)mod2 <-lm(P ~ S + New, data=house.selling.price.2)mod3 <-lm(P ~ S + New + Ba, data=house.selling.price.2)mod4 <-lm(P ~ .,data=house.selling.price.2)#A few with interaction variablesmod5 <-lm(P ~ S + New + S*New, data=house.selling.price.2)mod6 <-lm(P ~ S + New + Ba + S*New, data=house.selling.price.2)mod7 <-lm(P ~ . + S * New, data=house.selling.price.2)

###R2

Code

summary(mod1)$r.squared

[1] 0.807866

Code

summary(mod2)$r.squared

[1] 0.8483699

Code

summary(mod3)$r.squared

[1] 0.8681361

Code

summary(mod4)$r.squared

[1] 0.868863

Code

summary(mod5)$r.squared

[1] 0.8675196

Code

summary(mod6)$r.squared

[1] 0.8891938

Code

summary(mod7)$r.squared

[1] 0.8906193

Using ‘highest R-squared’ as our criteria, P ~ . + S * New is the winner. That one includes all the predictor variables in the equation, with size and newness as interaction variables.

###Adjusted R2

Code

summary(mod1)$adj.r.squared

[1] 0.8057546

Code

summary(mod2)$adj.r.squared

[1] 0.8450003

Code

summary(mod3)$adj.r.squared

[1] 0.8636912

Code

summary(mod4)$adj.r.squared

[1] 0.8629022

Code

summary(mod5)$adj.r.squared

[1] 0.8630539

Code

summary(mod6)$adj.r.squared

[1] 0.8841571

Code

summary(mod7)$adj.r.squared

[1] 0.8843331

Adjusted R-squared penalizes for adding more explanatory variables to the regression. However, it is still a virtual tie between P ~ S + New + Ba + S*New and P ~ . + S * New. Still, the latter wins.

###PRESS

This elegant function is found on Github and requires no additional libraries.

Code

PRESS <-function(linear.model) {#' calculate the predictive residuals pr <-residuals(linear.model)/(1-lm.influence(linear.model)$hat)#' calculate the PRESS PRESS <-sum(pr^2)return(PRESS)}

According to a comparison of the PRESS statistics, the best model is P ~ S + New + Ba + S*New with a PRESS of 27501.78

Code

PRESS(mod1)

[1] 38203.29

Code

PRESS(mod2)

[1] 31066

Code

PRESS(mod3)

[1] 27860.05

Code

PRESS(mod4)

[1] 28390.22

Code

PRESS(mod5)

[1] 31899.8

Code

PRESS(mod6)

[1] 27501.78

Code

PRESS(mod7)

[1] 27665.14

###AIC

According to AIC, the best (lowest) score is 774.9558, associated with the model P ~ S + New + Ba + S*New

Code

AIC(mod1)

[1] 820.1439

Code

AIC(mod2)

[1] 800.1262

Code

AIC(mod3)

[1] 789.1366

Code

AIC(mod4)

[1] 790.6225

Code

AIC(mod5)

[1] 789.5704

Code

AIC(mod6)

[1] 774.9558

Code

AIC(mod7)

[1] 775.7515

###BIC

According to BIC, the best model is the same - P ~ S + New + Ba + S*New, with a statistic of 790.1514.

Code

BIC(mod1)

[1] 827.7417

Code

BIC(mod2)

[1] 810.2566

Code

BIC(mod3)

[1] 801.7996

Code

BIC(mod4)

[1] 805.8181

Code

BIC(mod5)

[1] 802.2334

Code

BIC(mod6)

[1] 790.1514

Code

BIC(mod7)

[1] 793.4797

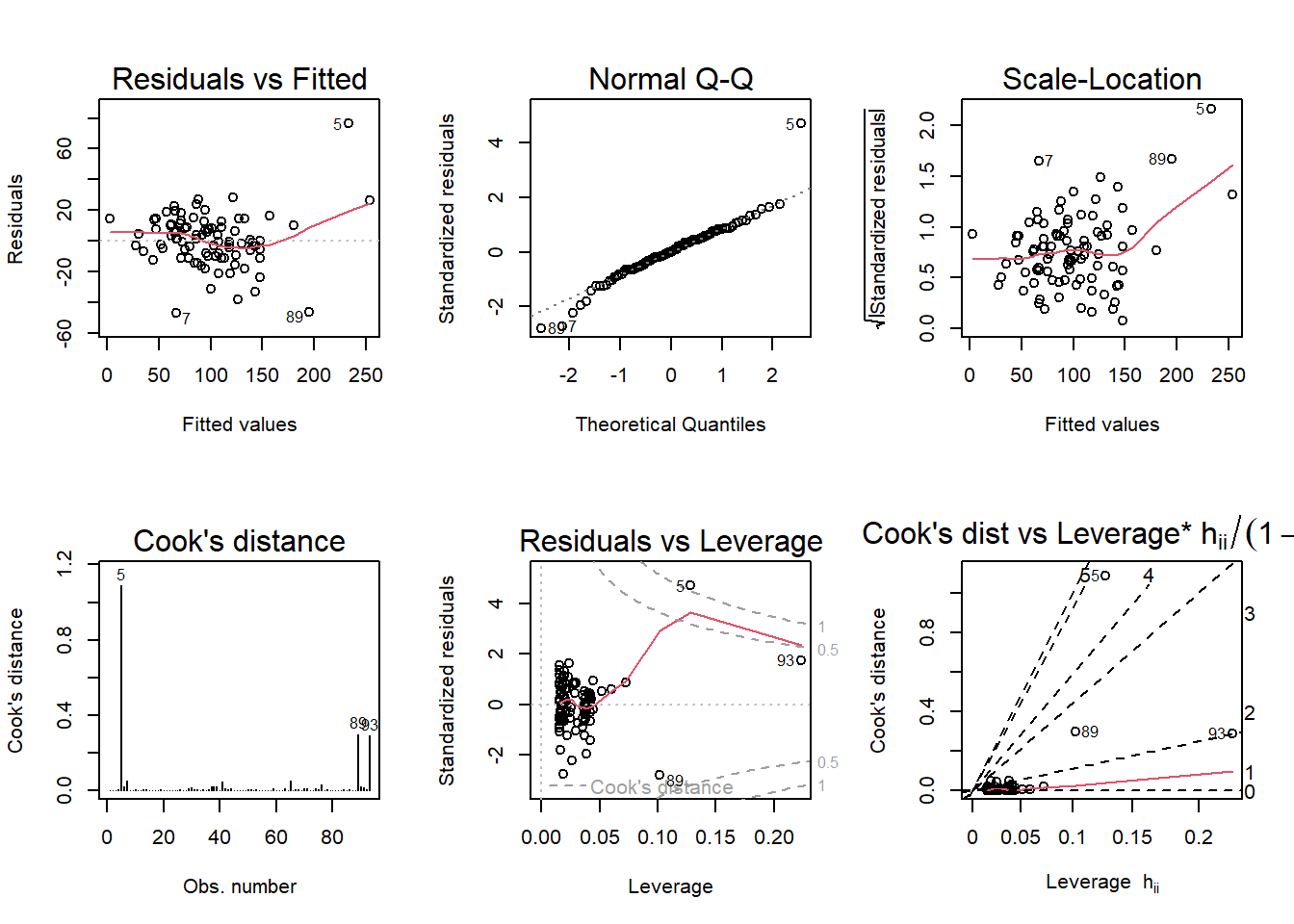

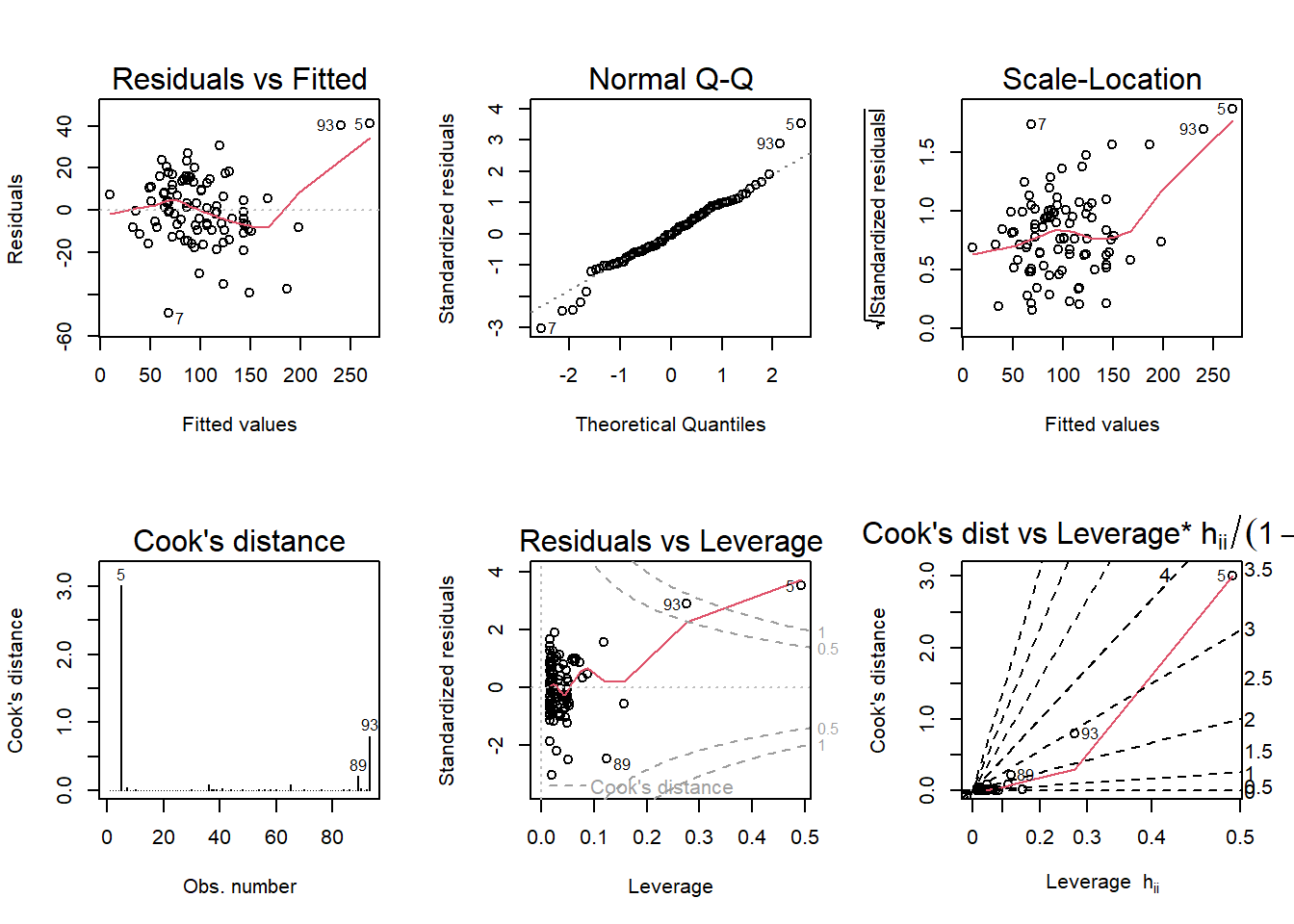

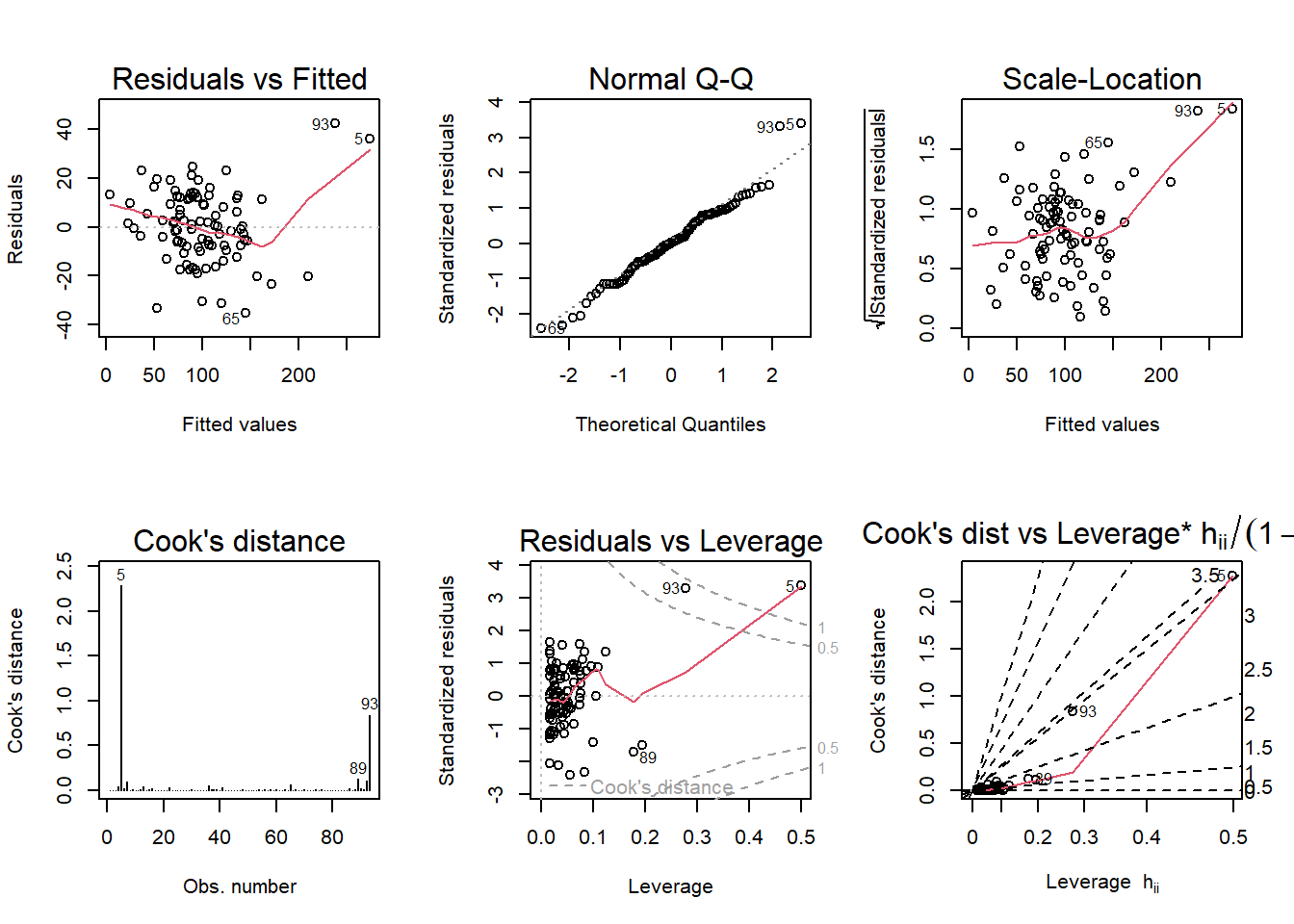

Explain which model you prefer and why.

I prefer the model favored by AIC and BIC, P ~ S + New + Ba + S*New. Intuitively, it makes sense that bedrooms are not a significant driver of a house’s price, although bathrooms are. And the size of a house is more consequential on the outcome of price when the building is newer.

From the documentation: “This data set provides measurements of the diameter, height and volume of timber in 31 felled black cherry trees. Note that the diameter (in inches) is erroneously labeled Girth in the data. It is measured at 4 ft 6 in above the ground.”

Tree volume estimation is a big deal, especially in the lumber industry. Use the trees data to build a basic model of tree volume prediction. In particular,

fit a multiple regression model with the Volume as the outcome and Girth and Height as the explanatory variables

Code

mod8 <-lm(Volume ~ Girth + Height, data = trees)

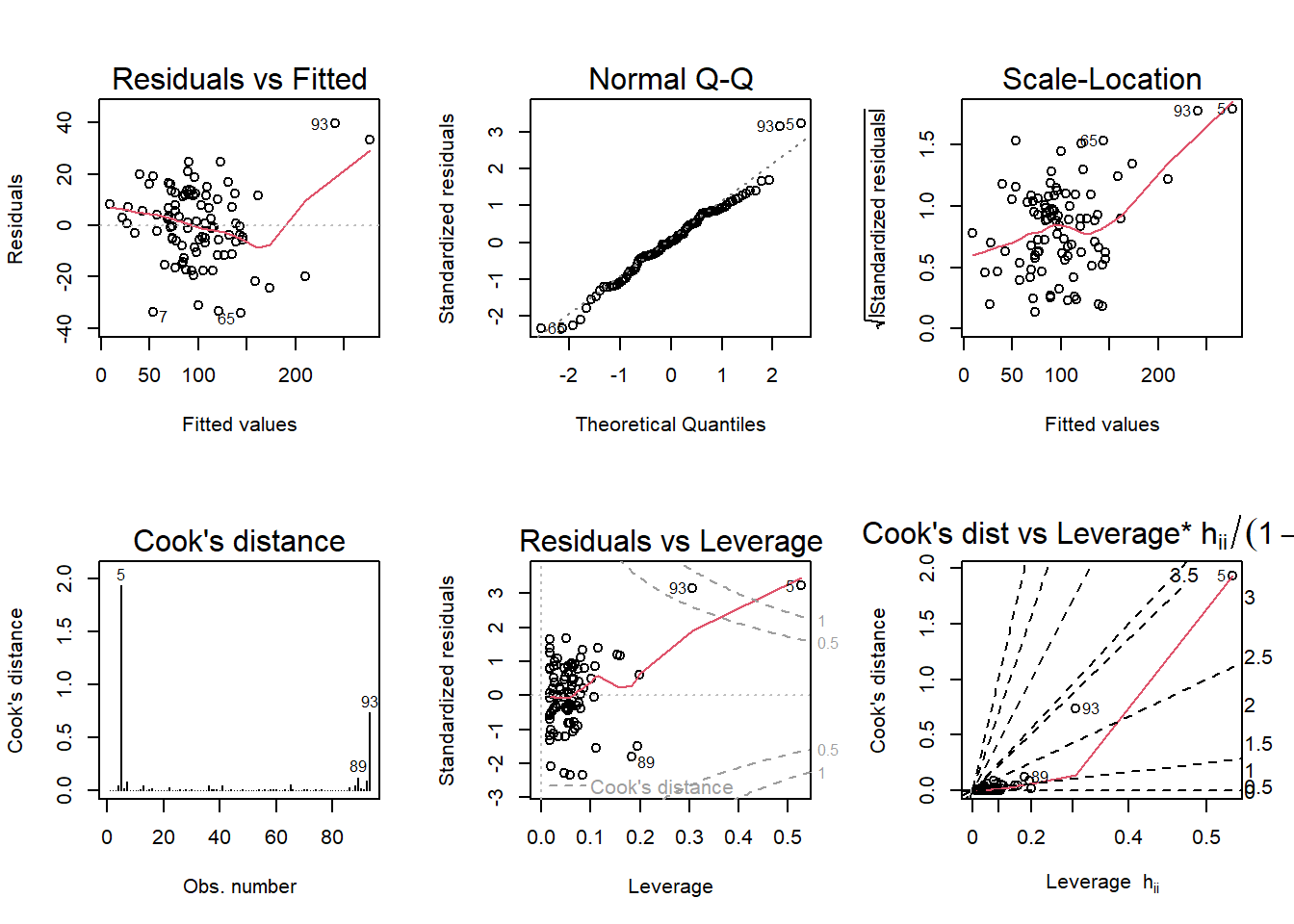

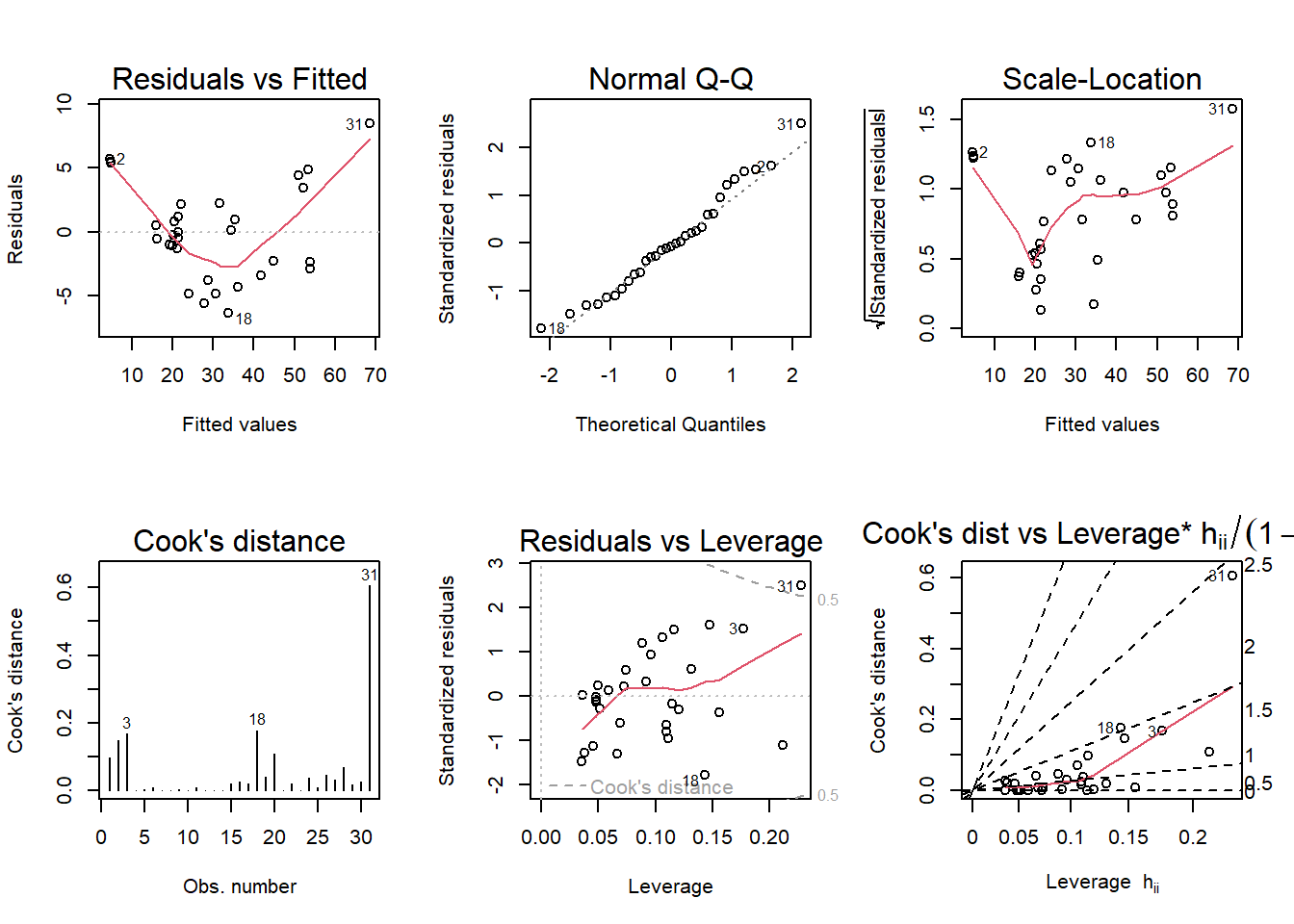

Run regression diagnostic plots on the model. Based on the plots, do you think any of the regression assumptions is violated?

These plots show some significant issues with the regression Volume ~ Girth + Height.

The ‘Residuals vs Fitted’ graph is U-shaped, indicating an issue with linearity.

The Normal Q-Q graph actually looks pretty good except for a wild outlier - this shows an issue with normality.

The Scale-Location graph should also be flat, but isn’t. This indicates an issue with homoscedasticity.

The Cook’s distance graph shows a clear outlier in one of the observations. A ‘high leverage’ observation (above the benchmark of 1 or n/4) may effect the regression if it were taken out.

The Residuals vs Leverage plot and Cook’s dist vs Leverage plot also show the influence of this outlier.

Code

par(mfrow =c(2,3)); plot(mod8, which =1:6)

Question 3

In the 2000 election for U.S. president, the counting of votes in Florida was controversial. In Palm Beach County in south Florida, for example, voters used a so-called butterfly ballot. Some believe that the layout of the ballot caused some voters to cast votes for Buchanan when their intended choice was Gore.

Code

florida

Gore Bush Buchanan

ALACHUA 47300 34062 262

BAKER 2392 5610 73

BAY 18850 38637 248

BRADFORD 3072 5413 65

BREVARD 97318 115185 570

BROWARD 386518 177279 789

CALHOUN 2155 2873 90

CHARLOTTE 29641 35419 182

CITRUS 25501 29744 270

CLAY 14630 41745 186

COLLIER 29905 60426 122

COLUMBIA 7047 10964 89

DADE 328702 289456 561

DE SOTO 3322 4256 36

DIXIE 1825 2698 29

DUVAL 107680 152082 650

ESCAMBIA 40958 73029 504

FLAGLER 13891 12608 83

FRANKLIN 2042 2448 33

GADSDEN 9565 4750 39

GILCHRIST 1910 3300 29

GLADES 1420 1840 9

GULF 2389 3546 71

HAMILTON 1718 2153 24

HARDEE 2341 3764 30

HENDRY 3239 4743 22

HERNANDO 32644 30646 242

HIGHLANDS 14152 20196 99

HILLSBOROUGH 166581 176967 836

HOLMES 2154 4985 76

INDIAN RIVER 19769 28627 105

JACKSON 6868 9138 102

JEFFERSON 3038 2481 29

LAFAYETTE 788 1669 10

LAKE 36555 49963 289

LEE 73560 106141 305

LEON 61425 39053 282

LEVY 5403 6860 67

LIBERTY 1011 1316 39

MADISON 3011 3038 29

MANATEE 49169 57948 272

MARION 44648 55135 563

MARTIN 26619 33864 108

MONROE 16483 16059 47

NASSAU 6952 16404 90

OKALOOSA 16924 52043 267

OKEECHOBEE 4588 5058 43

ORANGE 140115 134476 446

OSCEOLA 28177 26216 145

PALM BEACH 268945 152846 3407

PASCO 69550 68581 570

PINELLAS 199660 184312 1010

POLK 74977 90101 538

PUTNAM 12091 13439 147

ST. JOHNS 19482 39497 229

ST. LUCIE 41559 34705 124

SANTA ROSA 12795 36248 311

SARASOTA 72854 83100 305

SEMINOLE 58888 75293 194

SUMTER 9634 12126 114

SUWANNEE 4084 8014 108

TAYLOR 2647 4051 27

UNION 1399 2326 26

VOLUSIA 97063 82214 396

WAKULLA 3835 4511 46

WALTON 5637 12176 120

WASHINGTON 2796 4983 88

Code

mod9 <-lm(Buchanan ~ Bush, data = florida)summary(mod9)

Call:

lm(formula = Buchanan ~ Bush, data = florida)

Residuals:

Min 1Q Median 3Q Max

-907.50 -46.10 -29.19 12.26 2610.19

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 4.529e+01 5.448e+01 0.831 0.409

Bush 4.917e-03 7.644e-04 6.432 1.73e-08 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 353.9 on 65 degrees of freedom

Multiple R-squared: 0.3889, Adjusted R-squared: 0.3795

F-statistic: 41.37 on 1 and 65 DF, p-value: 1.727e-08

Code

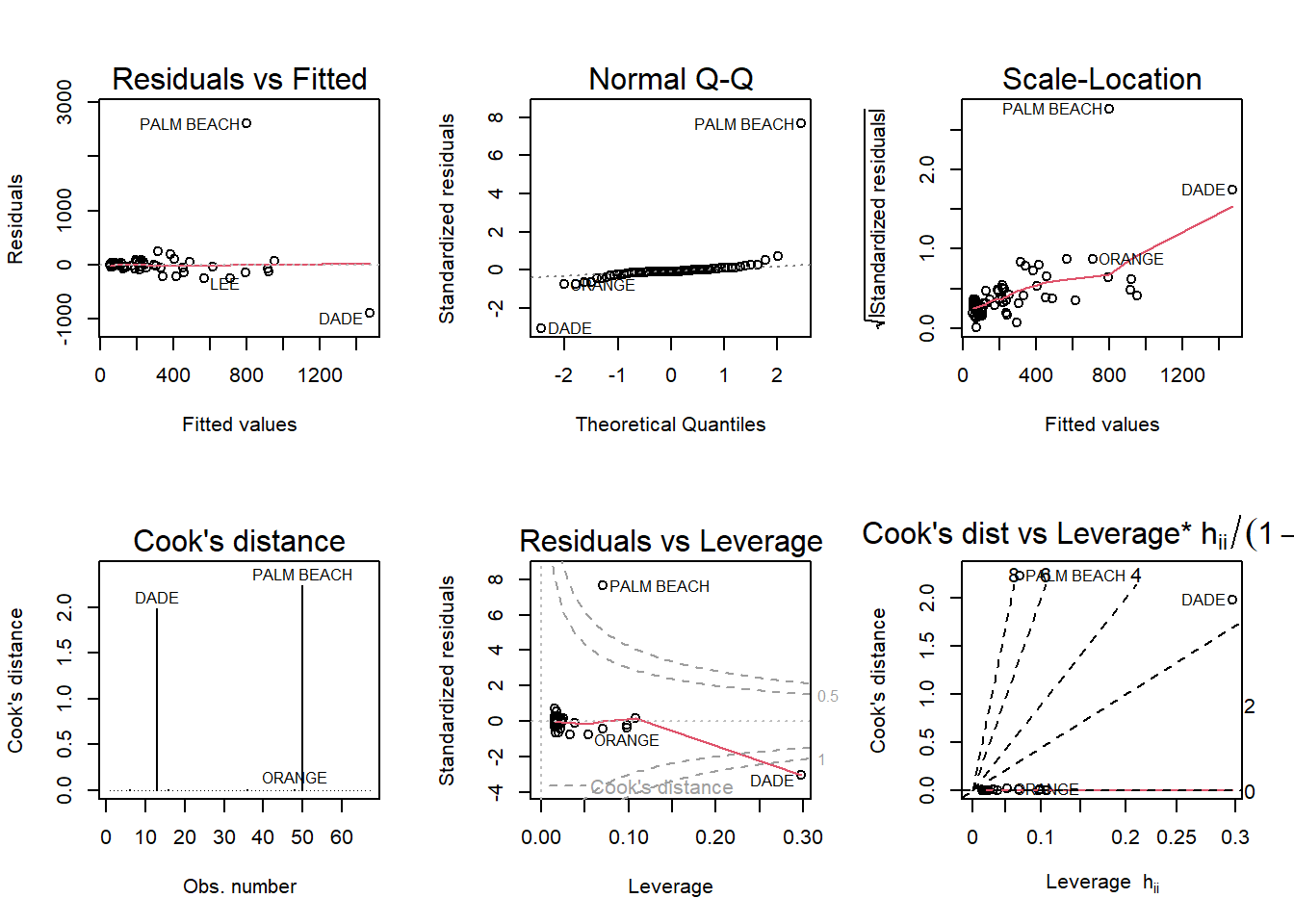

par(mfrow =c(2,3)); plot(mod9, which =1:6)

The normal Q-Q shows a strong outlier: Palm Beach county. It is very high in the Cook’s distance plot (over 1) and outside of the second dotted gray line in the Residuals vs Leverage plot.

Code

mod10 <-lm(log(Buchanan) ~log(Bush), data = florida)summary(mod10)

Call:

lm(formula = log(Buchanan) ~ log(Bush), data = florida)

Residuals:

Min 1Q Median 3Q Max

-0.96075 -0.25949 0.01282 0.23826 1.66564

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -2.57712 0.38919 -6.622 8.04e-09 ***

log(Bush) 0.75772 0.03936 19.251 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.4673 on 65 degrees of freedom

Multiple R-squared: 0.8508, Adjusted R-squared: 0.8485

F-statistic: 370.6 on 1 and 65 DF, p-value: < 2.2e-16

Logging both variables increased the coefficient, lowered the p-value of log(Bush), and increased the multiple R-squared by almost half. The findings of the first model are better-supported.

Source Code

---title: "Homework 5"author: "Steve O'Neill"description: "Homework 5"date: "11/27/2022"df-paged: trueformat: html: toc: true code-fold: true code-copy: true code-tools: truecategories: - hw5---```{r}library(smss)library(tidyverse)data(house.selling.price.2)library(alr4)data("florida")```*For the house.selling.price.2 data the tables below show a correlation matrix and a model fit using four predictors of selling price.*In this data, the variables are meant as:`P`: selling price`Be`: number of bedrooms`Ba`: number of bathrooms`New`: whether new (1 = yes, 0 = no)Here is my impression of the correlation matrix:```{r}cor(house.selling.price.2)```And regression output:```{r}fit <-lm(P ~ ., data=house.selling.price.2)summary(fit)```## Automated variable selection*For backward elimination, which variable would be deleted first? Why?*If I was doing backward elimination, I would pick a significance level (let's say alpha = .05) and, at each stage, delete the variable with the largest p-value. I would stop when all variables are significant.In this example, I would delete the `Be` (bedroom) variable.```{r}summary(lm(P ~ . - Be, data=house.selling.price.2))```*For forward selection, which variable would be added first? Why?*Like backward elimination, I would also predetermine a significance level (say, 5%). But here I would begin with no explanatory variable.The `Size` variable would be added first in forward selection.```{r}intercept_only <-lm(P ~1, data=house.selling.price.2)step(intercept_only, direction ="forward", scope=~ S + Be + Ba + New)```*Why do you think that BEDS has such a large P-value in the multiple regression model, even though it has a substantial correlation with PRICE?*As pointed out, `Be` does have a substantial correlation with `P` at .59. However, the large P-values in multiple regression indicate that while holding other variables fixed, it does not 'explain' the response variable of `P`, price.*Using software with these four predictors, find the model that would be selected using each criterion:*I'm not sure if I exactly get the question, but I will arbitrarily compare some models that I have made from combinations of the predictors.```{r}mod1 <-lm(P ~ S, data=house.selling.price.2)mod2 <-lm(P ~ S + New, data=house.selling.price.2)mod3 <-lm(P ~ S + New + Ba, data=house.selling.price.2)mod4 <-lm(P ~ .,data=house.selling.price.2)#A few with interaction variablesmod5 <-lm(P ~ S + New + S*New, data=house.selling.price.2)mod6 <-lm(P ~ S + New + Ba + S*New, data=house.selling.price.2)mod7 <-lm(P ~ . + S * New, data=house.selling.price.2)```###R2```{r}summary(mod1)$r.squaredsummary(mod2)$r.squaredsummary(mod3)$r.squaredsummary(mod4)$r.squaredsummary(mod5)$r.squaredsummary(mod6)$r.squaredsummary(mod7)$r.squared```Using 'highest R-squared' as our criteria, `P ~ . + S * New` is the winner. That one includes all the predictor variables in the equation, with size and newness as interaction variables.###Adjusted R2```{r}summary(mod1)$adj.r.squaredsummary(mod2)$adj.r.squaredsummary(mod3)$adj.r.squaredsummary(mod4)$adj.r.squaredsummary(mod5)$adj.r.squaredsummary(mod6)$adj.r.squaredsummary(mod7)$adj.r.squared```Adjusted R-squared penalizes for adding more explanatory variables to the regression. However, it is still a virtual tie between `P ~ S + New + Ba + S*New` and `P ~ . + S * New`. Still, the latter wins. ###PRESSThis elegant function is found on [Github](https://gist.github.com/tomhopper/8c204d978c4a0cbcb8c0) and requires no additional libraries.```{r}PRESS <-function(linear.model) {#' calculate the predictive residuals pr <-residuals(linear.model)/(1-lm.influence(linear.model)$hat)#' calculate the PRESS PRESS <-sum(pr^2)return(PRESS)}```According to a comparison of the PRESS statistics, the best model is `P ~ S + New + Ba + S*New` with a PRESS of 27501.78```{r}PRESS(mod1)PRESS(mod2)PRESS(mod3)PRESS(mod4)PRESS(mod5)PRESS(mod6)PRESS(mod7)```###AICAccording to AIC, the best (lowest) score is 774.9558, associated with the model `P ~ S + New + Ba + S*New````{r}AIC(mod1)AIC(mod2)AIC(mod3)AIC(mod4)AIC(mod5)AIC(mod6)AIC(mod7)```###BICAccording to BIC, the best model is the same - `P ~ S + New + Ba + S*New`, with a statistic of 790.1514.```{r}BIC(mod1)BIC(mod2)BIC(mod3)BIC(mod4)BIC(mod5)BIC(mod6)BIC(mod7)```*Explain which model you prefer and why.*I prefer the model favored by AIC and BIC, `P ~ S + New + Ba + S*New`. Intuitively, it makes sense that bedrooms are not a significant driver of a house's price, although bathrooms are. And the size of a house is more consequential on the outcome of price when the building is newer.```{r}par(mfrow =c(2,3)); plot(mod2, which =1:6)par(mfrow =c(2,3)); plot(mod5, which =1:6)par(mfrow =c(2,3)); plot(mod6, which =1:6)par(mfrow =c(2,3)); plot(mod7, which =1:6)```# Question 2```{r}data(trees)trees```*From the documentation: "This data set provides measurements of the diameter, height and volume of timber in 31 felled black cherry trees. Note that the diameter (in inches) is erroneously labeled Girth in the data. It is measured at 4 ft 6 in above the ground."**Tree volume estimation is a big deal, especially in the lumber industry. Use the trees data to build a basic model of tree volume prediction. In particular, **fit a multiple regression model with the Volume as the outcome and Girth and Height as the explanatory variables*```{r}mod8 <-lm(Volume ~ Girth + Height, data = trees)```*Run regression diagnostic plots on the model. Based on the plots, do you think any of the regression assumptions is violated?*These plots show some significant issues with the regression `Volume ~ Girth + Height`. 1. The 'Residuals vs Fitted' graph is U-shaped, indicating an issue with linearity. 2. The Normal Q-Q graph actually looks pretty good except for a wild outlier - this shows an issue with normality.3. The Scale-Location graph should also be flat, but isn't. This indicates an issue with homoscedasticity.4. The Cook's distance graph shows a clear outlier in one of the observations. A 'high leverage' observation (above the benchmark of 1 or n/4) may effect the regression if it were taken out.5. The Residuals vs Leverage plot and Cook's dist vs Leverage plot also show the influence of this outlier.```{r}par(mfrow =c(2,3)); plot(mod8, which =1:6)```# Question 3*In the 2000 election for U.S. president, the counting of votes in Florida was controversial. In Palm Beach County in south Florida, for example, voters used a so-called butterfly ballot. Some believe that the layout of the ballot caused some voters to cast votes for Buchanan when their intended choice was Gore.*```{r}florida``````{r}mod9 <-lm(Buchanan ~ Bush, data = florida)summary(mod9)par(mfrow =c(2,3)); plot(mod9, which =1:6)```The normal Q-Q shows a strong outlier: Palm Beach county. It is very high in the Cook's distance plot (over 1) and outside of the second dotted gray line in the Residuals vs Leverage plot. ```{r}mod10 <-lm(log(Buchanan) ~log(Bush), data = florida)summary(mod10)```Logging both variables increased the coefficient, lowered the p-value of log(Bush), and increased the multiple R-squared by almost half. The findings of the first model are better-supported.